The Speed of Obsolescence

What Norway's gas stations, China's battery manufacturers, and a stark climate change warning have in common

Three seemingly unrelated stories caught my attention over the past few weeks. At first glance, they appear to be about different industries—transportation, energy storage, and insurance. But they're actually revealing the same fundamental pattern: when systems reach tipping points, assets become stranded faster than anyone expects and the financial implications can cascade beyond the immediate sector.

From Everywhere to Nowhere

Tech futurist Michael Barnard has spent a considerable amount of time thinking about electric vehicles (EVs) and how their growing market share will impact many of the sights commonplace across global cities and highways - gas stations and car repair shops.

To illustrate his point, he examines Norway, and writes:

As EV sales move past 40%, gasoline stations begin closing at an accelerated pace. In Norway, EVs already represent over 90% of new car sales, and total fleet electrification is projected to approach 80% by the early 2030s. Gasoline stations, once plentiful, will soon become scarce. Remaining fuel stations will mainly exist along major highways or serve niche markets such as remote rural areas.

Essentially, the infrastructure that seemed permanent just five years ago is at risk of becoming economically nonviable.

Meanwhile, in China, battery energy storage system (BESS) manufacturers are locked in tight competition to produce cheaper, more efficient balance of systems. Think of a balance of system as essentially everything that goes into a battery energy storage system besides the battery - imagine large shipping containers with the wiring, inverters, transformers, and cooling systems that allow stored energy to flow to where it’s needed.

In late 2023, the Chinese government implemented a new standard forcing domestic companies to move from a 20-foot 3MWh container standard to a 5MWh standard. As Chinese companies began manufacturing at scale, the price of these 5MWh containers quickly dropped, making other, less energy dense models noncompetitive. Just a year and a half later, European companies were forced to drop their customized 3MWh designs and switch to producing the now industry standard 5MWh containers.

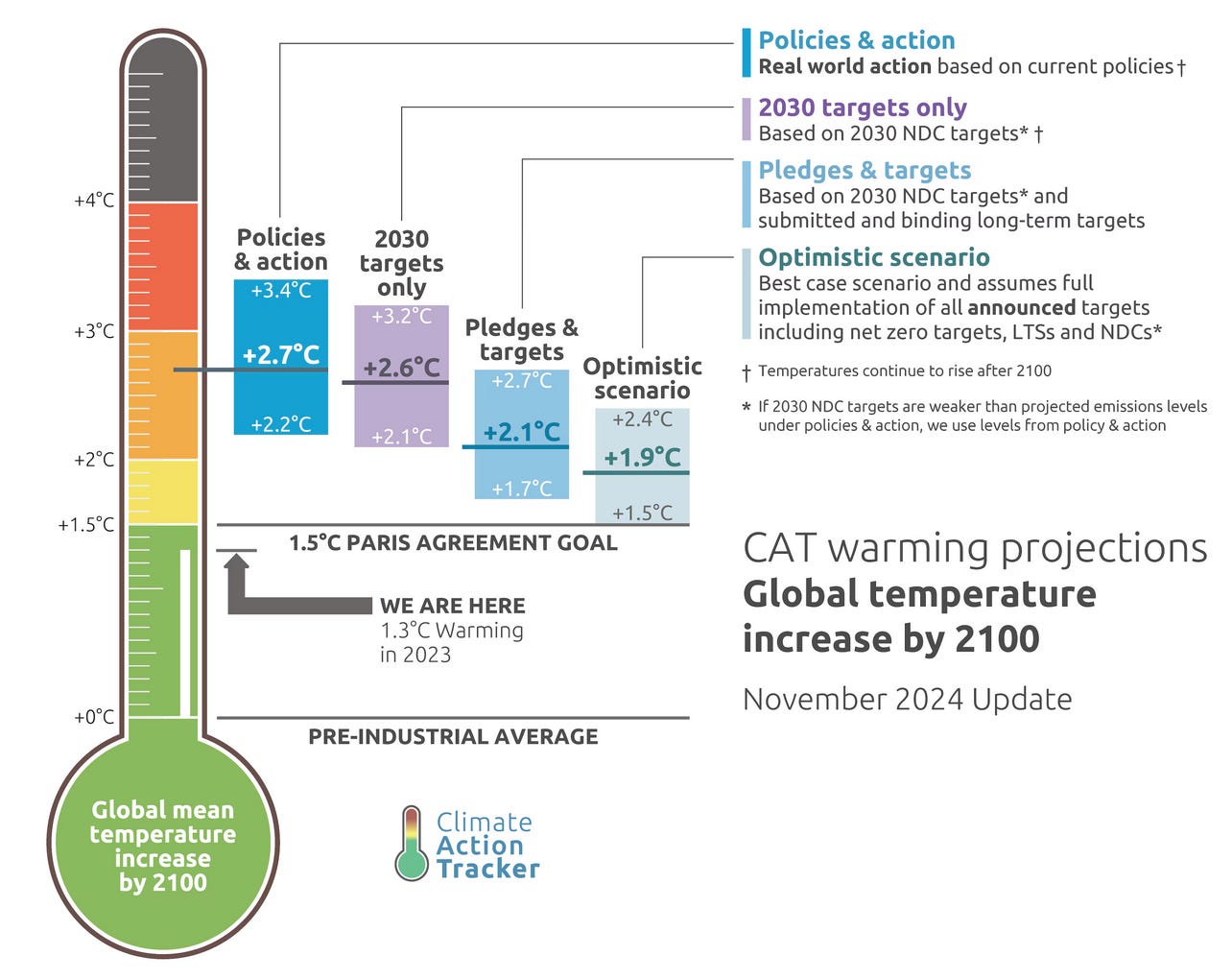

Finally, in March, Günther Thallinger from Allianz—one of the world's largest insurers—delivered a stark warning regarding the insurance industry and its ability to maintain coverage in the face of rising temperatures:

…we are fast approaching temperature levels—1.5°C, 2°C, 3°C—where insurers will no longer be able to offer coverage for many of these risks. The math breaks down: the premiums required exceed what people or companies can pay. This is already happening. Entire regions are becoming uninsurable. (emphasis mine)

This is not a one-off market adjustment. This is a systemic risk that threatens the very foundation of the financial sector. If insurance is no longer available, other financial services become unavailable too. A house that cannot be insured cannot be mortgaged. No bank will issue loans for uninsurable property. Credit markets freeze. This is a climate-induced credit crunch.

As Thallinger chillingly warns us, large swathes of the globe may soon be uninsurable, rendering an entire industry obsolete and unable to provide the coverage necessary for people to live in areas with increasing risks of storms, flooding, and wildfires.

When systems reach tipping points, assets become stranded faster than anyone expects, and the financial implications cascade far beyond the immediate sector.

The Math of Sudden Obsolescence

These aren't isolated examples of technological disruption. They reveal a pattern: transitions don't follow smooth, predictable curves. Instead, they hit tipping points where entire systems flip rapidly from viable to obsolete. The economic math changes so quickly that even sophisticated market participants get caught off guard.

The energy storage example is particularly telling. Container manufacturers aren't just competing on price—they're in a race where falling behind on energy density by 12-18 months can eliminate your market position entirely. When balance-of-system costs become the majority of project expenses, fitting more energy in the same container isn't an incremental improvement; it's a 60% cost reduction that makes competing technologies economically nonviable.

Planning For Yesterday’s Tomorrow

Working with utilities, government agencies, and technology companies, I've seen how easy it is for planners to assume gradual, linear change. Utilities model steady adoption curves, insurance companies price based on historical claims data, and manufacturers plan product life cycles in predictable sequences. But tipping point dynamics don't follow these patterns - especially given the speed of climate change, the urgency of the energy transition, and the rapidly increasing demand for new energy generation and storage systems.

Norway's ongoing transition to EVs will provide a useful test for how traditional internal combustion engine (ICE) infrastructure such as gas stations and repair shops will adapt (or not) in the face of rapid change. As this same dynamic plays out globally, urban planners and transportation analysts will have an interesting set of data on which to base their future predictions.

When the Numbers Stop Adding Up

The insurance industry's warning is perhaps most sobering because it's explicitly about financial system limits, not technological constraints. Thallinger isn't saying climate adaptation is technically impossible—he's saying it becomes economically impossible. When risks exceed the mathematical capacity of financial instruments to price and distribute them, the system stops functioning.

This connects to a broader pattern across infrastructure transitions: the financial implications often outpace the technological or operational changes. Battery storage density improvements create immediate obsolescence not because the old technology stops working, but because the economics shift so dramatically that financing and market viability disappear.

Infrastructure at the Speed of Disruption

What these examples reveal is that infrastructure planning in rapidly evolving sectors requires fundamentally different thinking. Instead of asking "How do we optimize current systems?" the question becomes "What happens when the current system becomes obsolete faster than we expect?"

For energy storage manufacturers, this means product development cycles measured in months, not years. For utilities planning grid investments, it means considering scenarios where distributed energy resources scale faster than central infrastructure can adapt. For policymakers, it means recognizing that insurance market failure at 3°C warming isn't just a climate issue—it's a financial system issue that could make economic planning itself impossible.

The pattern across all three sectors is clear: when systems reach tipping points, gradual transition assumptions become dangerous. The question isn't whether your infrastructure will become obsolete—it's whether you're planning for the speed at which obsolescence can occur.

The challenge isn't just technological innovation—it's building systems resilient enough to handle the economics of rapid obsolescence.